Topic 1: EQUITY: BULL ASSAULT

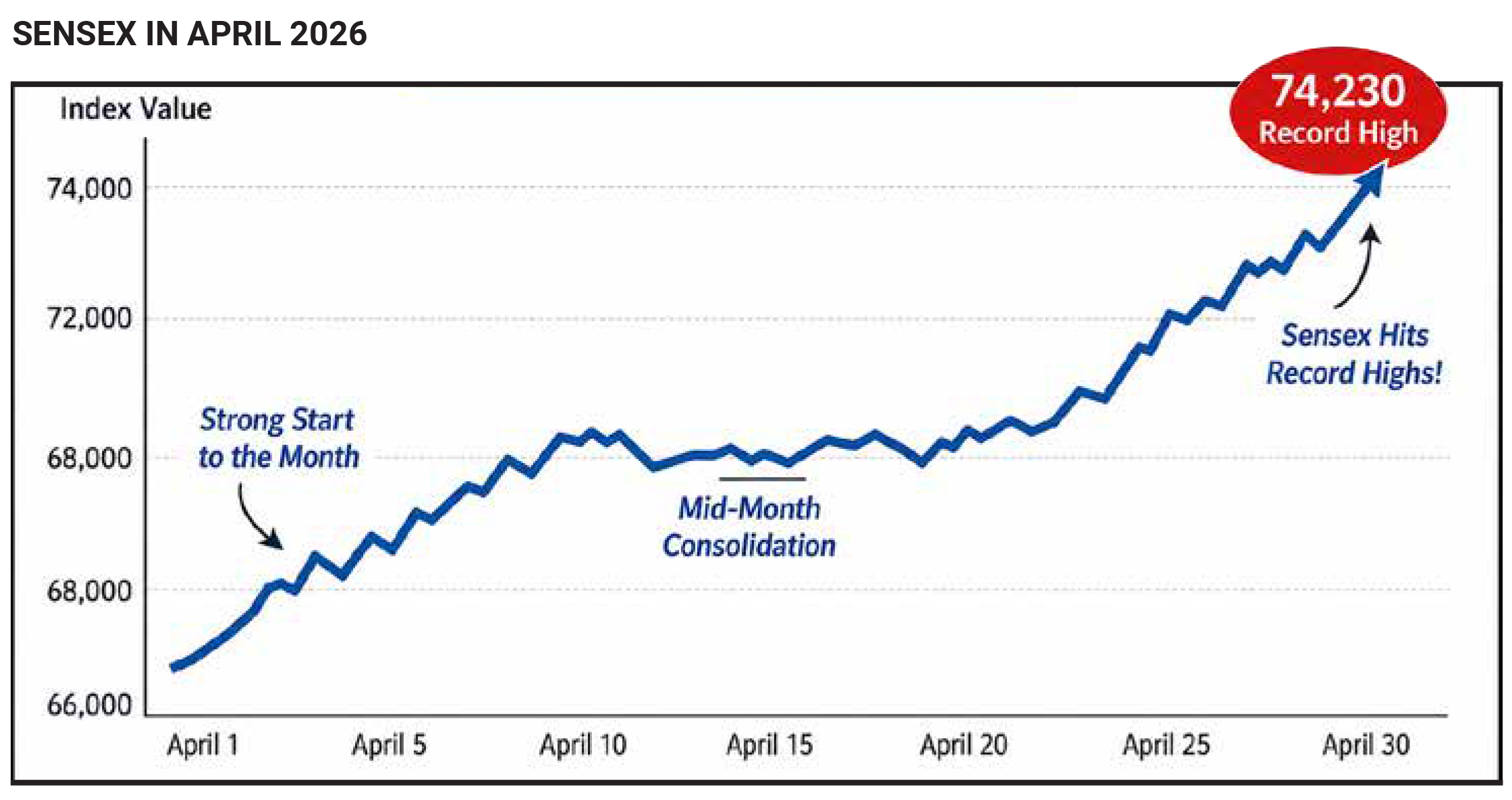

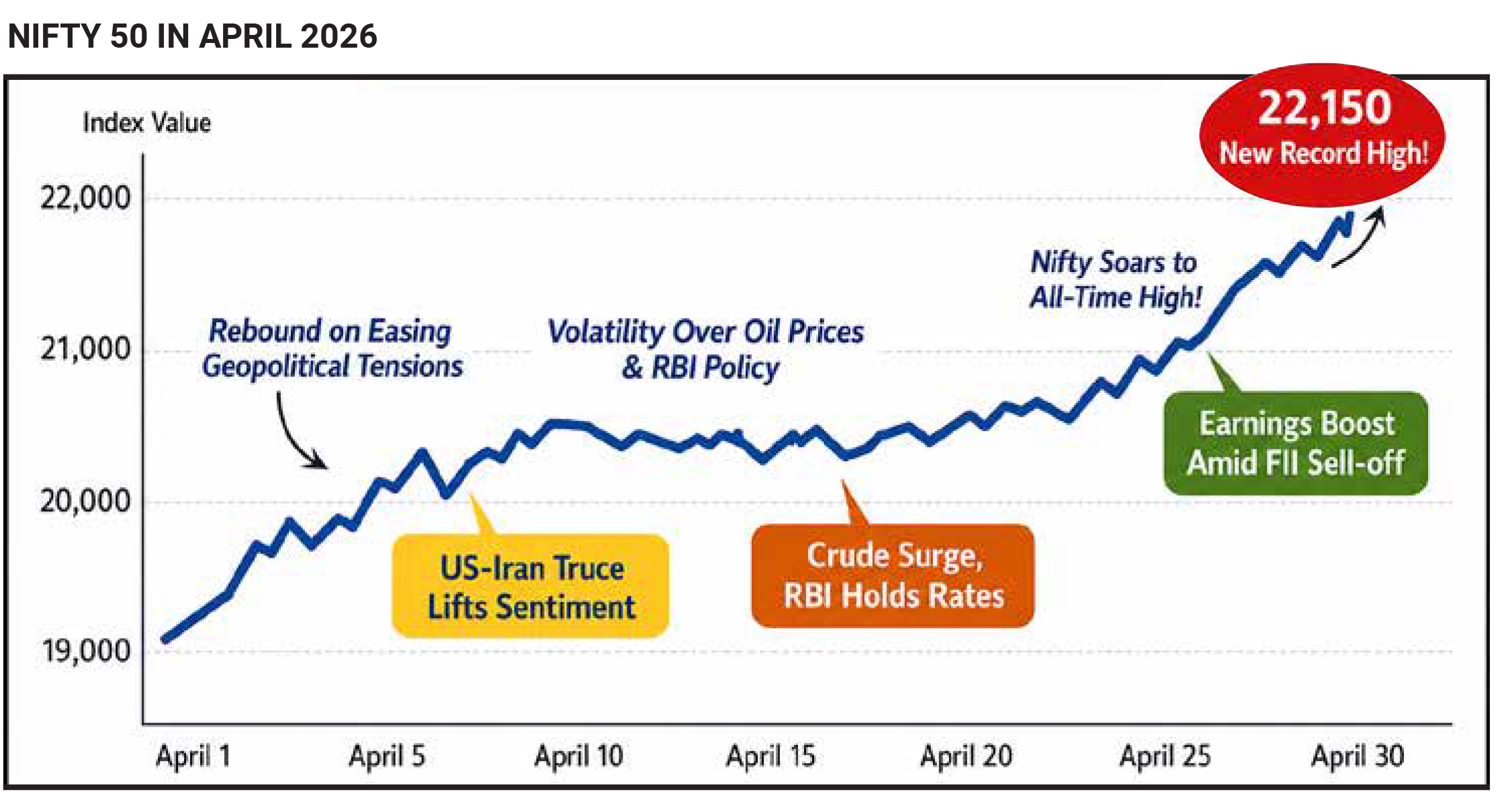

April 2026 marked a powerful turnaround for Indian equity markets, with benchmark indices staging their strongest monthly rally in nearly 28 months after the sharp correction witnessed in March. The Nifty 50 surged by 7.46% during the month, while the BSE Sensex climbed 6.90%, reversing a significant portion of the more than 11% decline recorded in the previous month. This recovery was not just limited to index performance; it was also reflected in a dramatic expansion of overall market wealth. The total market capitalization of all domestically listed companies jumped by nearly ₹51 trillion, reaching an unprecedented ₹463.3 trillion—marking the highest absolute monthly addition ever recorded in Indian market history and surpassing the previous peak increase of ₹28.9 trillion seen in March 2025. The scale and speed of this rebound highlighted the resilience of domestic markets despite persistent global uncertainties and continued selling pressure from foreign investors.

The beginning of April, however, was far from optimistic.

Markets opened the month on a weak note, with indices

declining sharply due to heightened geopolitical

tensions, elevated crude oil prices, and aggressive

foreign institutional investor (FII) outflows. On April 2, the

indices dropped more than 2% in a single session,

reflecting widespread panic triggered by escalating

conflict in West Asia, particularly involving the United

States and Iran. This geopolitical shock had already

rattled markets in March, pushing Brent crude oil prices

above $100 per barrel and intensifying concerns over

inflation, current account deficits, and monetary

tightening in India. However, as the month progressed,

sentiment began to gradually shift. By mid-April, reports

of a ceasefire or de-escalation in tensions between the

United States and Iran helped restore confidence in

global markets. This easing of geopolitical risk acted as

a major catalyst for the rebound in Indian equities.

One of the most crucial macroeconomic variables

influencing market behaviour during this period was

crude oil. India, being a major importer of oil, is highly

sensitive to fluctuations in global crude prices. In early

April, Brent crude hovered in the range of $106–110 per

barrel, raising fears of imported inflation and potential

policy tightening by the Reserve Bank of India. However,

as geopolitical tensions eased, crude prices stabilised

and began to soften slightly, reducing the immediate

pressure on the Indian economy. By early May, Brent

crude had eased to around $107.9 per barrel, providing

further relief to investors. This stabilisation played a key

role in improving sentiment, particularly in rate-sensitive

sectors such as banking, automobiles, and real estate,

which had been heavily impacted during the March

sell-off.

Another important factor shaping market dynamics was

global monetary policy, especially the stance of the

Federal Reserve. Amid rising inflation risks linked to

geopolitical developments, the Federal Reserve chose to

keep interest rates unchanged, while also signalling that

rate cuts in 2026 were unlikely. This created intermittent

pressure on global equity markets, including India, as

higher-for-longer interest rates tend to reduce liquidity

and dampen risk appetite. Despite this, Indian markets

demonstrated relative resilience, supported by strong

domestic fundamentals and investor participation.

Sectoral trends also played a significant role in driving

the April rally. In the latter half of the month, strong

buying was observed in sectors such as fast-moving

consumer goods (FMCG), automobiles, and real estate.

Leading companies including ITC Limited, Tech

Mahindra, Maruti Suzuki, and Reliance Industries

emerged as key contributors to index gains. The

performance of the automobile sector was particularly

noteworthy, supported by strong domestic demand data.

For instance, Maruti Suzuki reported record domestic

sales of 1,91,122 units in April 2026, compared to

1,42,053 units in April 2025, signalling robust

consumption trends and boosting investor confidence in

cyclical sectors.

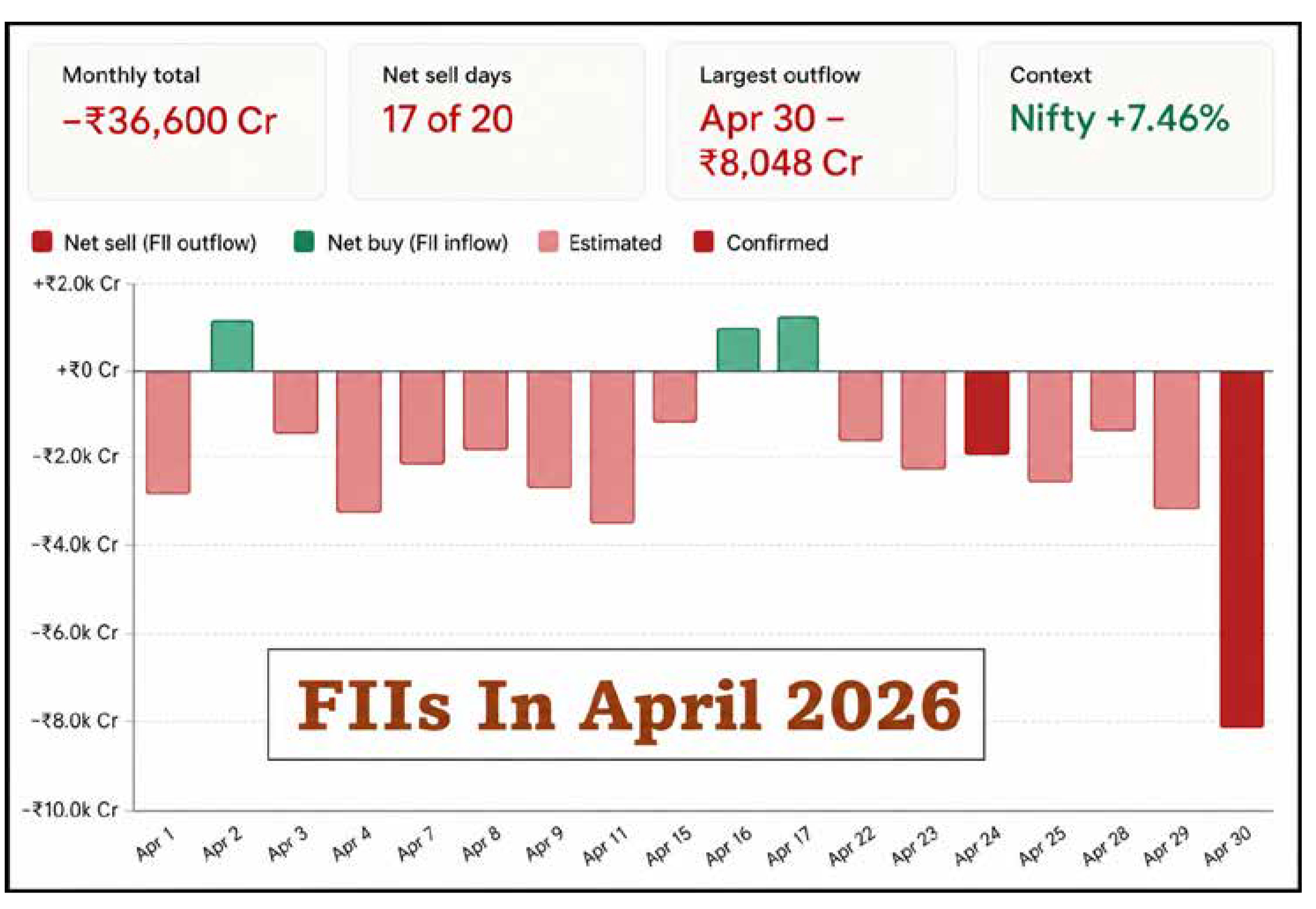

Despite these positive developments, the underlying

market structure remained complex due to the

divergence between foreign and domestic investor

behaviour. FIIs continued to be aggressive sellers

throughout April, offloading equities worth

approximately ₹43,000–44,000 crore in the cash

segment. This sustained selling was a continuation of

the heavy outflows seen in March and reflected global

risk aversion, currency pressures, and relatively more

attractive yields in developed markets. Under normal

circumstances, such persistent FII selling would have

exerted significant downward pressure on the indices.

However, this time, domestic institutional investors

(DIIs) and retail participants played a crucial

counterbalancing role. DIIs invested over ₹34,000 crore

during the month, while steady inflows from retail

investors—particularly through systematic investment

plans (SIPs)—provided additional support. This created

a dynamic “tug of war” in the market, where FII selling

dragged indices down while DII and retail buying helped

stabilise and eventually push them higher.

Liquidity conditions and currency stability further

contributed to the positive momentum. While the Indian

rupee remained under pressure, it did not experience any

sharp or disorderly depreciation. The Reserve Bank of

India’s liquidity management measures, combined with

consistent domestic inflows, prevented any systemic

stress in financial markets. This stability allowed the

broader “India growth story”—characterised by strong

consumption, infrastructure development, and a robust

capital expenditure cycle—to regain prominence in

investor narratives. Public sector undertakings (PSUs)

and promoter-driven companies saw renewed interest

during the rally.

By the end of April 2026, the Sensex was trading in the

range of approximately 77,500 to 78,500, while the Nifty

settled between 24,100 and 24,400, marking a

substantial recovery from their March lows. The

momentum carried into early May as well. On May 4,

2026, after ending the previous week on a weak note,

markets opened strongly, with the Sensex rising over 997

points to touch 77,910 and the Nifty gaining 292 points to

reach 24,290 in early trade. However, investor sentiment

remained somewhat cautious due to the ongoing state

election results, which had the potential to influence

short-term market direction.

In summary, April 2026 represented a classic case of a

sharp correction followed by a strong technical and

sentiment-driven rebound. The recovery was fuelled by

easing geopolitical tensions, stabilising crude oil prices,

supportive domestic economic data, and strong

participation from domestic investors. Even though

foreign investors remained net sellers throughout the

period, their impact was effectively absorbed by

domestic flows, allowing the market to post its best

monthly performance in over two years. The interplay

between global uncertainties and domestic resilience

defined the market narrative, reinforcing the importance

of internal demand and liquidity in sustaining India’s

equity market momentum.