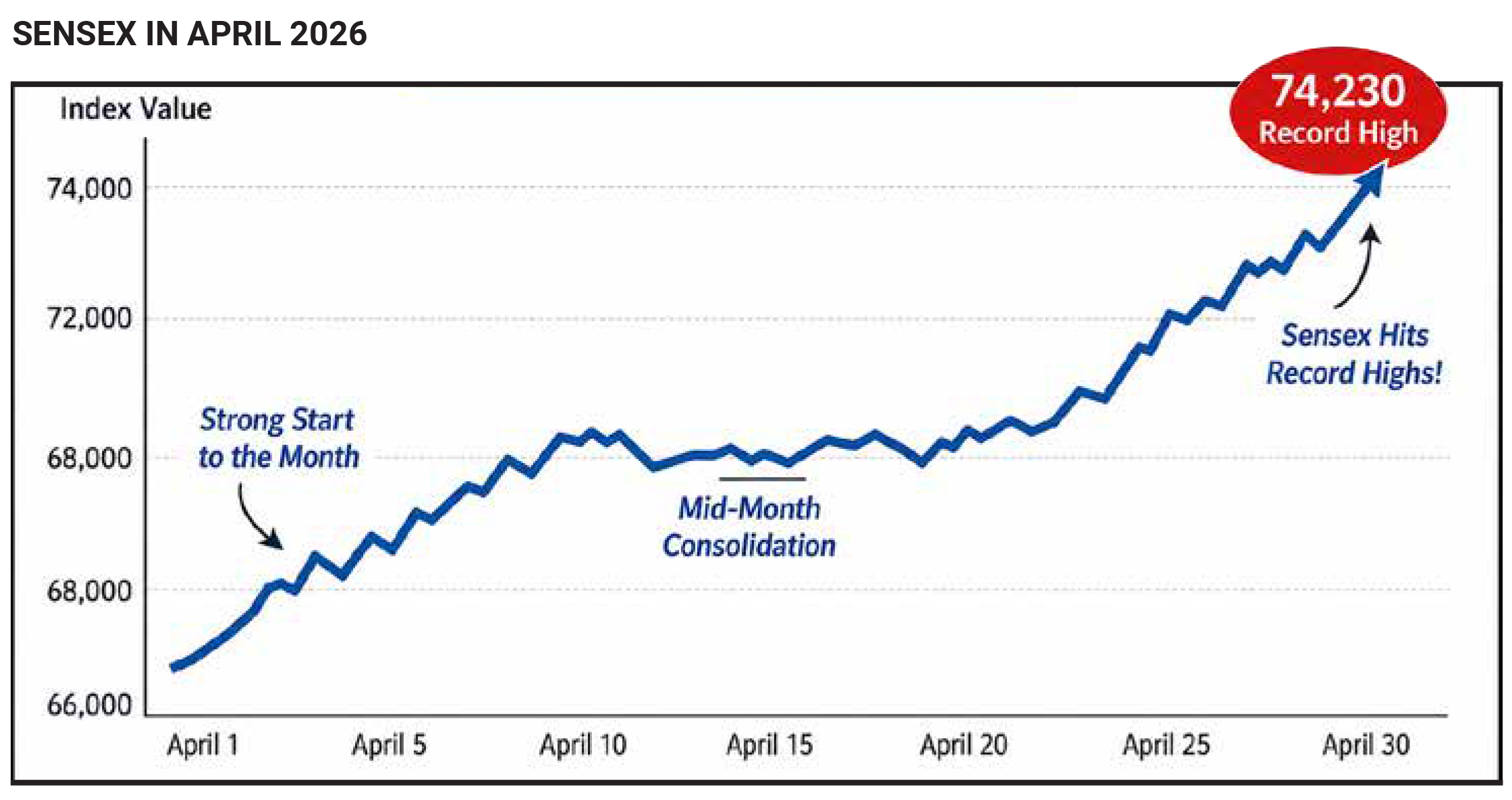

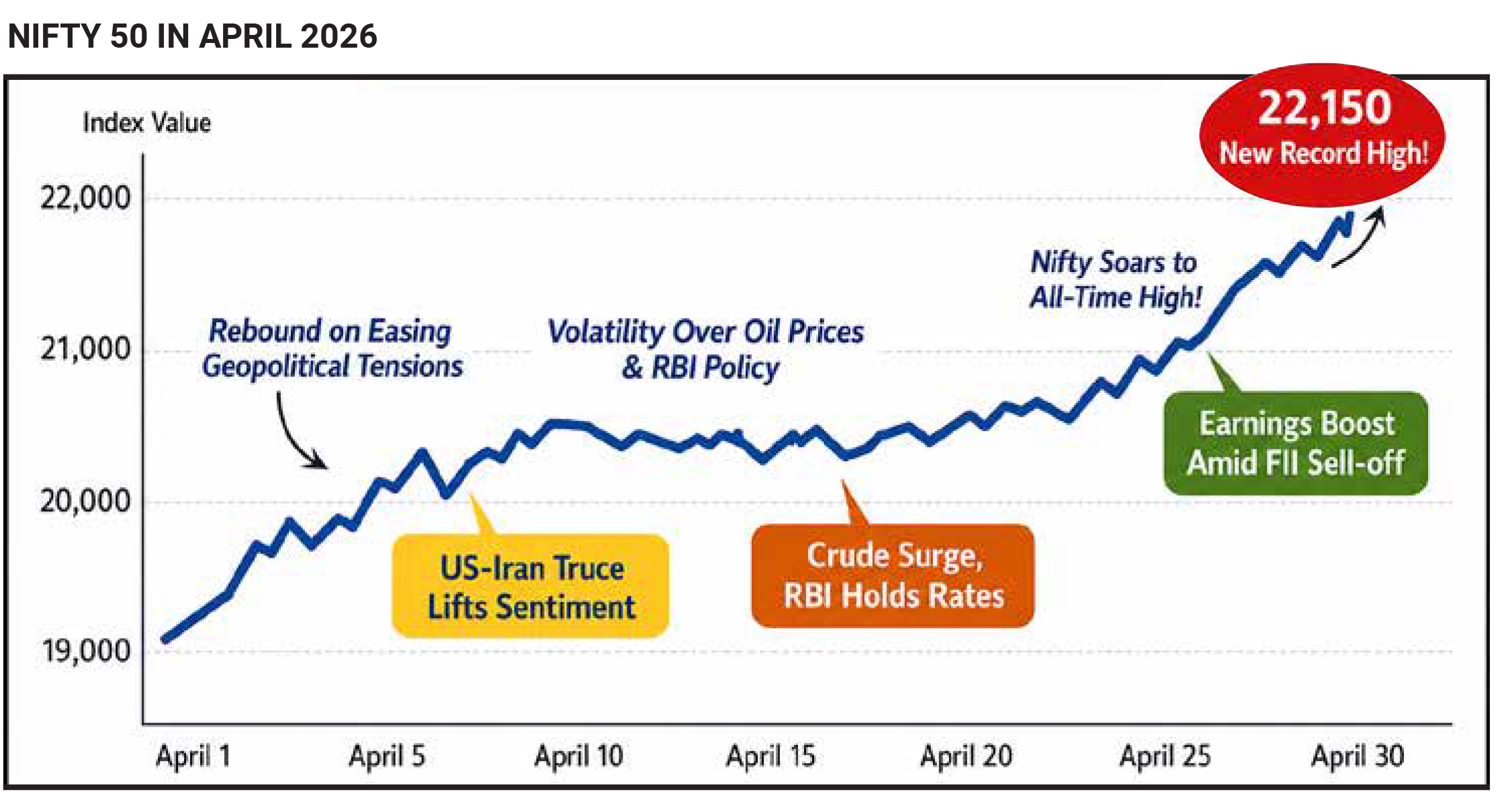

April 2026 marked a powerful turnaround for Indian equity markets, with benchmark indices staging their strongest monthly rally in nearly 28 months after the sharp correction witnessed in March. The Nifty 50 surged by 7.46% during the month, while the BSE Sensex climbed 6.90%, reversing a significant portion of the more than 11% decline recorded in the previous month. This recovery was not just limited to index performance; it was also reflected in a dramatic expansion of overall market wealth. The total market capitalization of all domestically listed companies jumped by nearly ₹51 trillion, reaching an unprecedented ₹463.3 trillion—marking the highest absolute monthly addition ever recorded in Indian market history and surpassing the previous peak increase of ₹28.9 trillion seen in March 2025. The scale and speed of this rebound highlighted the resilience of domestic markets despite persistent global uncertainties and continued selling pressure from foreign investors.

The beginning of April, however, was far from optimistic.

Markets opened the month on a weak note, with indices

declining sharply due to heightened geopolitical

tensions, elevated crude oil prices, and aggressive

foreign institutional investor (FII) outflows. On April 2, the

indices dropped more than 2% in a single session,

reflecting widespread panic triggered by escalating

conflict in West Asia, particularly involving the United

States and Iran. This geopolitical shock had already

rattled markets in March, pushing Brent crude oil prices

above $100 per barrel and intensifying concerns over

inflation, current account deficits, and monetary

tightening in India. However, as the month progressed,

sentiment began to gradually shift. By mid-April, reports

of a ceasefire or de-escalation in tensions between the

United States and Iran helped restore confidence in

global markets. This easing of geopolitical risk acted as

a major catalyst for the rebound in Indian equities.

One of the most crucial macroeconomic variables

influencing market behaviour during this period was

crude oil. India, being a major importer of oil, is highly

sensitive to fluctuations in global crude prices. In early

April, Brent crude hovered in the range of $106–110 per

barrel, raising fears of imported inflation and potential

policy tightening by the Reserve Bank of India. However,

as geopolitical tensions eased, crude prices stabilised

and began to soften slightly, reducing the immediate

pressure on the Indian economy. By early May, Brent

crude had eased to around $107.9 per barrel, providing

further relief to investors. This stabilisation played a key

role in improving sentiment, particularly in rate-sensitive

sectors such as banking, automobiles, and real estate,

which had been heavily impacted during the March

sell-off.

Another important factor shaping market dynamics was

global monetary policy, especially the stance of the

Federal Reserve. Amid rising inflation risks linked to

geopolitical developments, the Federal Reserve chose to

keep interest rates unchanged, while also signalling that

rate cuts in 2026 were unlikely. This created intermittent

pressure on global equity markets, including India, as

higher-for-longer interest rates tend to reduce liquidity

and dampen risk appetite. Despite this, Indian markets

demonstrated relative resilience, supported by strong

domestic fundamentals and investor participation.

Sectoral trends also played a significant role in driving

the April rally. In the latter half of the month, strong

buying was observed in sectors such as fast-moving

consumer goods (FMCG), automobiles, and real estate.

Leading companies including ITC Limited, Tech

Mahindra, Maruti Suzuki, and Reliance Industries

emerged as key contributors to index gains. The

performance of the automobile sector was particularly

noteworthy, supported by strong domestic demand data.

For instance, Maruti Suzuki reported record domestic

sales of 1,91,122 units in April 2026, compared to

1,42,053 units in April 2025, signalling robust

consumption trends and boosting investor confidence in

cyclical sectors.

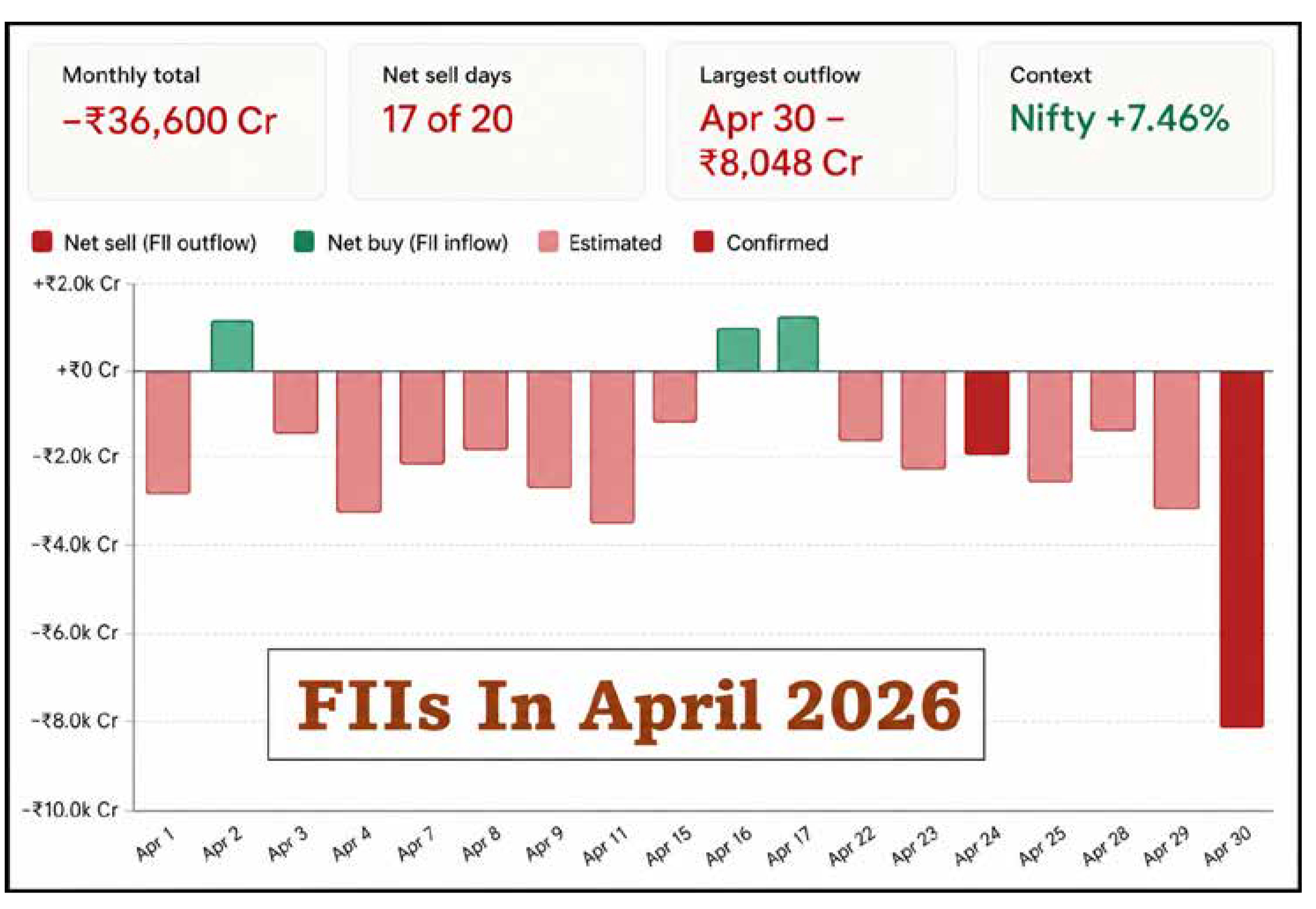

Despite these positive developments, the underlying

market structure remained complex due to the

divergence between foreign and domestic investor

behaviour. FIIs continued to be aggressive sellers

throughout April, offloading equities worth

approximately ₹43,000–44,000 crore in the cash

segment. This sustained selling was a continuation of

the heavy outflows seen in March and reflected global

risk aversion, currency pressures, and relatively more

attractive yields in developed markets. Under normal

circumstances, such persistent FII selling would have

exerted significant downward pressure on the indices.

However, this time, domestic institutional investors

(DIIs) and retail participants played a crucial

counterbalancing role. DIIs invested over ₹34,000 crore

during the month, while steady inflows from retail

investors—particularly through systematic investment

plans (SIPs)—provided additional support. This created

a dynamic “tug of war” in the market, where FII selling

dragged indices down while DII and retail buying helped

stabilise and eventually push them higher.

Liquidity conditions and currency stability further

contributed to the positive momentum. While the Indian

rupee remained under pressure, it did not experience any

sharp or disorderly depreciation. The Reserve Bank of

India’s liquidity management measures, combined with

consistent domestic inflows, prevented any systemic

stress in financial markets. This stability allowed the

broader “India growth story”—characterised by strong

consumption, infrastructure development, and a robust

capital expenditure cycle—to regain prominence in

investor narratives. Public sector undertakings (PSUs)

and promoter-driven companies saw renewed interest

during the rally.

By the end of April 2026, the Sensex was trading in the

range of approximately 77,500 to 78,500, while the Nifty

settled between 24,100 and 24,400, marking a

substantial recovery from their March lows. The

momentum carried into early May as well. On May 4,

2026, after ending the previous week on a weak note,

markets opened strongly, with the Sensex rising over 997

points to touch 77,910 and the Nifty gaining 292 points to

reach 24,290 in early trade. However, investor sentiment

remained somewhat cautious due to the ongoing state

election results, which had the potential to influence

short-term market direction.

In summary, April 2026 represented a classic case of a

sharp correction followed by a strong technical and

sentiment-driven rebound. The recovery was fuelled by

easing geopolitical tensions, stabilising crude oil prices,

supportive domestic economic data, and strong

participation from domestic investors. Even though

foreign investors remained net sellers throughout the

period, their impact was effectively absorbed by

domestic flows, allowing the market to post its best

monthly performance in over two years. The interplay

between global uncertainties and domestic resilience

defined the market narrative, reinforcing the importance

of internal demand and liquidity in sustaining India’s

equity market momentum.

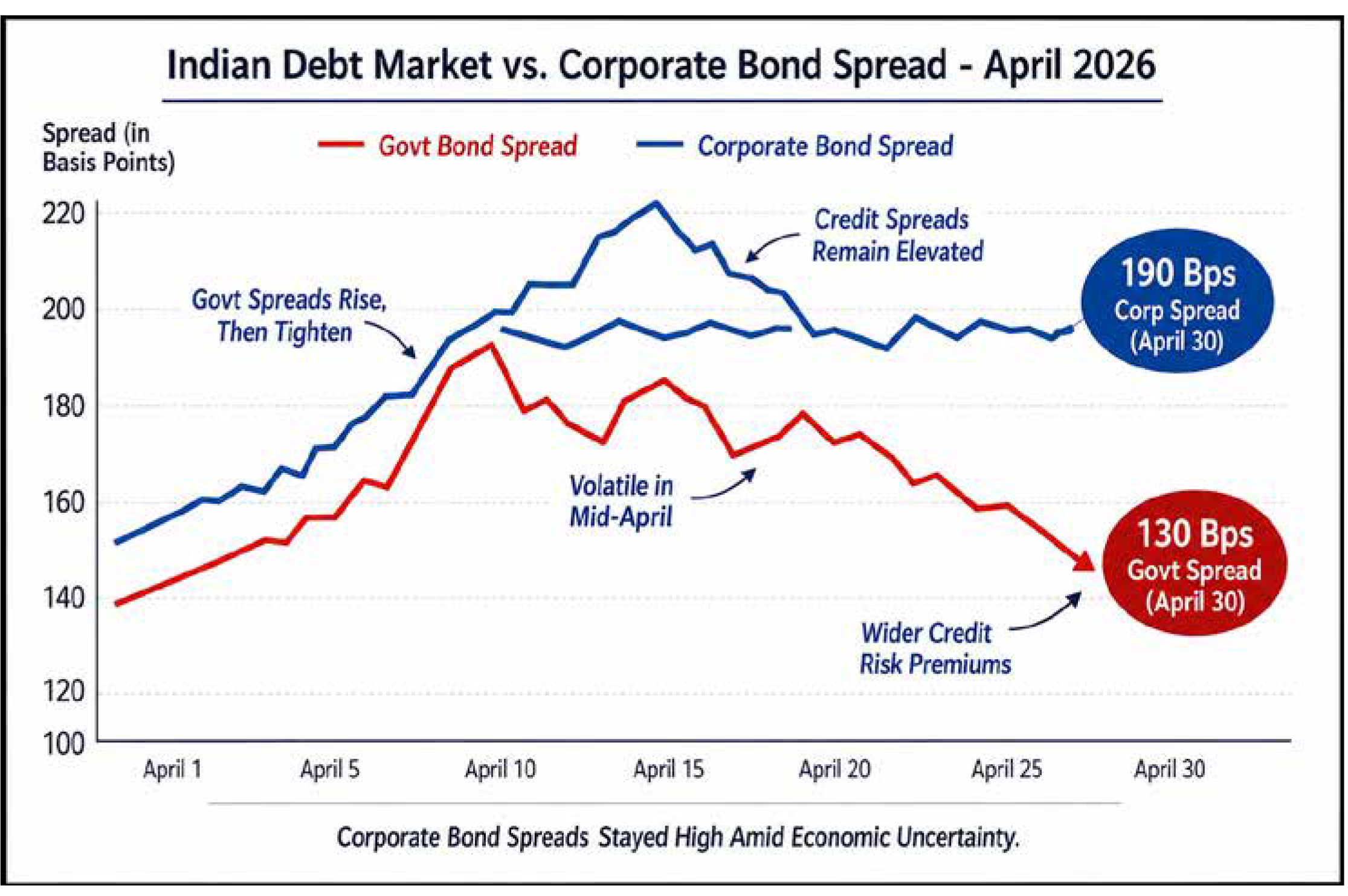

In April 2026, India’s debt markets faced a broad-based

selloff as yields repriced sharply upward in response to

geopolitical tensions in West Asia, rising crude oil prices,

and mounting inflation concerns. This environment

proved particularly challenging for interest

rate–sensitive instruments, especially government

securities (G-secs) and long-duration debt funds. As

yields climbed across the curve, bond prices declined,

leading to negative returns in several fixed-income

categories. However, the impact was not

uniform—shorter-duration instruments and

credit-oriented products displayed relative resilience,

supported by lower duration risk and stable credit

spreads.

Government securities bore the brunt of the adjustment.

The 10-year benchmark yield rose significantly, moving

from roughly 6.6–6.7% in early March to around

6.9–7.0% by late April, even touching a two-week high of

approximately 6.98% in mid-April. This upward

movement reflected a reassessment of inflation risks

and expectations of tighter monetary conditions.

Notably, the repricing was more pronounced at the short to mid-end of the yield curve. Yields on 2-year and 3-year

G-secs climbed steadily as markets began pricing in

near-term inflation pressures and the likelihood of

liquidity tightening by the Reserve Bank of India (RBI).

Similarly, 5-year bonds experienced upward pressure as

traders positioned for a less accommodative liquidity

environment. At the long end, 20- to 30-year bonds

underperformed further, as investors demanded higher

term premiums to compensate for fiscal uncertainties

and persistent inflation risks.

Corporate bond markets also reflected the broader

tightening in financial conditions, though with variations

across credit quality and sectors. Investment-grade

corporate bonds experienced moderate price pressure,

but in some cases, spreads tightened slightly, especially

in sectors linked to India’s capital expenditure cycle. This

resulted in largely flat to mildly negative returns for

top-rated instruments. In contrast, lower-rated or

high-yield bonds faced greater stress. Investors grew

increasingly cautious amid rising borrowing costs and

heightened volatility, leading to wider spreads and

weaker secondary market prices for these issuers.

Several interrelated factors drove these developments.

Foremost among them was the escalation of

geopolitical tensions in West Asia, which pushed Brent

crude oil prices sharply higher, in some instances

approaching or exceeding $100 per barrel. For an

oil-importing country like India, this translated into fears

of imported inflation, with potential knock-on effects on

both consumer and wholesale price indices. As inflation

expectations rose, markets began to anticipate a more

hawkish stance from the RBI, including the possibility of

prolonged higher policy rates. This led to a front-loading

of rate expectations, particularly impacting shorter-tenor

bonds.

At the same time, global bond markets experienced a

surge in volatility, reflected in rising rate volatility

indicators similar to the MOVE index. Yield curves

flattened globally, but at higher absolute levels, signalling

that investors were demanding greater compensation

for uncertainty. Indian bond markets followed suit, with

the rise in the 10-year yield reflecting not just inflation

expectations but also an increase in term premiums.

Liquidity and fiscal concerns further amplified the

upward pressure on yields. Expectations of tighter

domestic liquidity—driven by a higher import bill,

potential capital outflows during risk-off conditions, and

pressure on money market rates—made short-term

instruments more sensitive to rate changes. Meanwhile,

concerns about fiscal slippage, including higher

government spending on energy subsidies and possible

war-related expenditures, pushed long-term yields higher

as investors reassessed India’s fiscal trajectory.

Despite these pressures, the RBI played a stabilizing role

in the market. Through targeted open market operations

and secondary market purchases of government bonds,

the central bank helped anchor the 10-year yield,

preventing excessive volatility. However, this support

was concentrated around the benchmark segment,

leaving shorter- and longer-tenor bonds more exposed to

market-driven repricing.

Investor behaviour also influenced market outcomes.

Retail and institutional investors increasingly shifted

allocations toward shorter-duration and credit-focused

funds, seeking to mitigate interest rate risk. These flows

helped stabilize segments of the market and prevented a

disorderly selloff. However, investors with exposure to

long-duration gilt funds faced significant mark-to-market

losses, as rising yields eroded bond prices despite steady

coupon income.

In the corporate bond segment, yield movements closely

tracked changes in government bond yields but were

further influenced by credit risk considerations.

Top-rated AAA and A1 issuers saw yields rise by around

20–30 basis points, while BBB-rated and lower-quality

issuers experienced more substantial increases of

40–60 basis points or more. Sectoral differences were

also evident. Industries heavily dependent on crude oil or

global trade—such as aviation, shipping, refining, and

certain manufacturing segments—saw sharper yield

increases due to concerns about margin compression

and earnings volatility. Conversely , defensive sectors

like large public sector enterprises, regulated utilities,

and select financial institutions experienced more

moderate yield movements, supported by stable cash

flows and, in some cases, implicit government backing.

In essence, April 2026 underscored the vulnerability of

debt markets to external shocks and the critical

importance of duration management. While rising yields

created near-term pain through capital losses, they also

reset the yield environment to more attractive levels for

future investors, particularly in shorter-duration and

high-quality segments.

In April 2026, bullion markets—especially gold and

silver—moved within a broadly upward but highly volatile

range, shaped by geopolitical tensions, crude-driven

inflation fears, and evolving global monetary policy

expectations. Gold clearly outperformed, supported by

strong safe-haven demand and structural tailwinds,

while silver lagged due to its sensitivity to industrial

demand and macroeconomic uncertainty. The month

reflected a “risk-off but rate-sensitive” environment: gold

benefited from geopolitical stress but faced intermittent

pressure from higher interest rate expectations, whereas

silver struggled to sustain gains.

Gold prices in India and globally showed sharp swings

followed by consolidation. At the beginning of April,

domestic 24-karat gold was around ₹1,50,100 per 10

grams. However, on April 2, prices briefly dropped to

about ₹1,45,600 due to profit booking, a stronger US

dollar, and global liquidity pressures. This fall was

short-lived and largely technical, following a steep rally

linked to safe-haven demand. By mid-April (around April

17–19), gold surged to a monthly high near ₹1,55,000 per

10 grams, driven by escalating West Asia tensions, rising

crude oil prices, and seasonal demand during the

Akshaya Tritiya period. Toward the end of the month,

prices stabilized near ₹1,51,000 per 10 grams, leaving

gold modestly higher overall.

On MCX, gold futures reflected similar volatility. For

example, on April 14, June gold futures rose nearly ₹2,000

(about 1.3%) in a single session, highlighting rapid

sentiment shifts. Retail gold prices in Indian cities

remained strong, hovering around ₹15,400–₹15,500 per

gram at peak levels, indicating resilient domestic demand

despite high prices.

Silver, however, underperformed throughout April. It

initially traded around ₹2.64–2.65 lakh per kilogram in

mid-April but failed to sustain these levels. By late April,

prices fell to the ₹2.35–₹2.44 lakh range, reflecting

weaker momentum. This divergence widened the

gold–silver ratio, emphasizing gold’s strength as a

defensive asset compared to silver’s dual industrial and

precious metal role.

The primary driver of bullion movements was the

escalation of geopolitical tensions in West Asia,

particularly involving the US and Iran. These

developments triggered safe-haven buying, with analysts

estimating a “war risk premium” of about $10–15 per

ounce in gold prices. However, periodic ceasefire talks

led to profit booking, contributing to volatility.

Structural demand factors added further strength. Global

central banks continued to accumulate gold as part of

reserve diversification, while limited growth in mining

supply reinforced the tight supply narrative. Investor

flows also played a key role: gold ETFs saw strong

inflows globally and in India, as investors sought

protection against geopolitical and market risks. These

inflows helped gold resist deeper corrections.

Domestic factors in India further supported gold

prices. Seasonal demand from weddings and festivals,

especially around Akshaya Tritiya, sustained physical

buying even at high price levels. Jewellers maintained

firm premiums, limiting downside risks. Silver did not

benefit similarly, as its demand is more tied to

industrial activity, which weakened amid concerns

about slower global growth and higher interest rates.

The sharp fall on April 2 highlights the market’s

volatility. This drop was driven by a stronger US dollar,

profit booking after a rapid rally, and easing crude

prices. Additionally, geopolitical rhetoric initially

boosted the dollar, prompting liquidation of leveraged

gold positions. On MCX, prices briefly fell sharply

before recovering, indicating a technical correction

rather than a trend reversal.

Overall, April 2026 saw a volatile but upward-trending

bullion market. Gold remained resilient and

outperformed due to its safe-haven appeal,

inflation-hedging properties, and strong investment

demand. Silver lagged due to its industrial exposure

and sensitivity to macro tightening. The interplay of

geopolitical risks, crude prices, monetary policy, and

investor behaviour defined the market, reinforcing

gold’s role as a key defensive asset in uncertain times.

In April 2026, the Indian rupee (INR) experienced an

exceptionally volatile and weakening trend against the

US dollar (USD), driven primarily by external shocks

rather than domestic economic weakness. The currency

came under sustained pressure throughout the month,

reflecting a combination of surging crude oil prices,

geopolitical tensions in West Asia, global monetary

tightening, and significant capital outflows. While some

data points suggest extreme depreciation toward the

₹95 mark, the broader and more consistent market

narrative indicates that the rupee moved within a sharply

volatile but controlled depreciating range, weakening

from around ₹82.8–83.2 per USD in late March to

approximately ₹83.8–84.5 by the end of April. This made

April one of the most turbulent months for the rupee in

recent times, marked by sharp swings rather than a

one-directional collapse.

The rupee’s movement over the month reflected shifting

global sentiment. Early in April, the currency came under

pressure as crude oil prices surged and risk aversion

increased, pushing it past the ₹83 mark. Around

mid-April, there were brief phases of stabilization and

even mild recovery, supported by temporary easing in

geopolitical tensions and intervention by the Reserve

Bank of India. However, these gains proved short-lived,

and by the latter part of the month, the rupee weakened

again toward the ₹84+ zone as external pressures

persisted and demand for dollars remained strong.

Overall, the rupee displayed a pattern of high volatility

with a clear depreciation bias.

The primary driver of this weakness was the sharp rise in

crude oil prices due to escalating conflict in West Asia.

Brent crude surged toward $100–110 per barrel,

significantly increasing India’s import bill. As India

imports over 80–90% of its crude requirements, higher

oil prices led to a surge in demand for US dollars by oil

marketing companies to finance imports. This placed

direct downward pressure on the rupee and worsened

the current account deficit outlook, further weakening

currency sentiment.

Geopolitical tensions also triggered a global “risk-off”

environment. Investors shifted capital toward safe-haven

assets such as the US dollar and gold, leading to

outflows from emerging markets like India. Foreign

institutional investors (FIIs) pulled out substantial funds

from Indian equities and debt markets, intensifying dollar

demand and adding to rupee depreciation. This flight to

safety was reinforced by uncertainty surrounding global

trade routes and energy supply disruptions.

Another key factor was the strength of the US dollar,

supported by the US Federal Reserve’s “higher for

longer” interest rate stance. Elevated US yields attracted

global capital into US assets, reducing the relative

attractiveness of emerging market investments. This

narrowing of interest rate differentials exerted additional

pressure on the rupee, as capital moved away from India

toward safer, higher-yielding US instruments.

Inflation dynamics further compounded the situation.

Rising crude prices and a weakening rupee created a

feedback loop—higher oil costs increased imported

inflation, while a weaker currency made imports even

more expensive. This heightened concerns about

inflation in India and reduced expectations of monetary

easing, reinforcing the negative sentiment around the

rupee.

Despite these pressures, the RBI played a crucial

stabilizing role. It intervened actively in the foreign

exchange market by selling dollars from its reserves and

using liquidity tools to prevent excessive volatility. While

the central bank did not attempt to defend a specific

exchange rate level, its actions helped contain the

rupee’s depreciation within a manageable range and

avoided a disorderly. Some domestic factors also

provided limited support. Continued inflows from

domestic institutional investors, relatively stable

macroeconomic fundamentals, and steady foreign

direct investment and services exports helped cushion

the impact of external shocks. In summary, April 2026 was a pressure-heavy month for the rupee, shaped by a “perfect storm” of high oil prices, geopolitical uncertainty, global risk aversion, and strong US dollar dynamics. The rupee weakened under these external stresses but remained relatively stable compared to more severe scenarios, thanks to timely RBI intervention and underlying economic resilience.

In April 2026, crude oil prices experienced an

extraordinary and highly volatile surge, driven by a

combination of severe geopolitical disruptions, supply

shocks, and structural market tightness. Prices moved

from an already elevated base into a full-blown crisis

zone, with Brent crude rising from roughly $94–100 per

barrel at the start of the month to peak at an intraday

high of about $126.10 by April 30, while WTI crude

climbed to around $110.24. Even after some late-month

cooling, Brent remained elevated in the $108–112 range,

marking one of the sharpest monthly rallies in recent

years. Overall, crude followed a

“spike–pullback–consolidation” pattern, characterized

by extreme intraday volatility and rapid reactions to

geopolitical developments, ultimately ending the month

significantly higher than where it began.

The single most important driver behind this surge was

the near shutdown of the Strait of Hormuz, the world’s

most critical oil transit route. By late April, the strait was

functioning at only a fraction of its normal capacity,

effectively removing an estimated 8–10 million barrels

per day from global supply. This created an

unprecedented supply shock, as major producers in the

region—including Iraq, Saudi Arabia, and the UAE—were

unable to export oil safely. Tanker disruptions forced

rerouting around Africa, sharply increasing freight and

insurance costs and amplifying the price spike.

Geopolitical escalation further intensified the rally. The

deepening conflict involving the US, Israel, and

Iran—particularly the announcement of a naval blockade

against Iran—convinced markets that supply disruptions

would persist. Repeated threats and attacks on regional

energy infrastructure sustained a high “war premium” on

oil prices, with traders pricing in worst-case scenarios of

prolonged conflict. This geopolitical risk alone added an

estimated $10–20 per barrel to crude prices during peak

tension periods.

Another major factor was structural instability within the

global oil supply system. The unexpected exit of the

OPEC+ alliance by the UAE in late April weakened the

cartel’s ability to manage supply and maintain price

discipline. This move created uncertainty about future

production coordination and further destabilized market

expectations at a time when supply was already

constrained. Combined with existing production cuts

and limited spare capacity, the market had little buffer to

absorb shocks, making prices highly sensitive to

disruptions.

Demand-supply dynamics also played a critical role.

Global inventories were already low due to high refinery

utilization and limited stockpiling in late 2025. When

supply disruptions hit, there was insufficient buffer stock

to stabilize markets. Although high prices eventually led

to some demand destruction—particularly in sectors like

aviation and petrochemicals—the initial impact was a

sharp upward adjustment in prices as buyers rushed to

secure supply. Strategic petroleum reserve releases and

alternative supply routes helped partially offset the

deficit but were insufficient to fully stabilize the market.

Speculative activity amplified the price movements.

Hedge funds and commodity traders increased long

positions in crude futures, driving prices higher with

each escalation headline. At the same time, volatility

remained elevated, as any signs of diplomatic progress

triggered profit booking and temporary pullbacks. This

created a cycle of sharp rallies followed by corrections,

without fundamentally reversing the upward trend.

Toward the end of April, prices showed signs of

moderation due to emerging diplomatic efforts,

including initiatives to secure shipping routes and

modest production increases from remaining

producers. However, these measures only partially

eased supply concerns, and crude prices remained

elevated, reflecting a persistent risk premium.

In summary, April 2026 was a geopolitics-driven oil

shock. Prices surged not just because of actual supply

losses, but because of the fear of prolonged disruption

in critical energy corridors. Tight supply conditions,

weak inventories, cartel instability, and speculative flows

all magnified the impact, highlighting the fragility of

global oil markets and their sensitivity to geopolitical

risk.

April 2026 marked a landmark phase for the Indian mutual fund industry, characterized by strong performance, major regulatory reforms, and evolving product innovation. Equity mutual funds delivered exceptional returns during the month, with over 25 schemes generating more than 25% returns, driven largely by a sharp market rebound and sectoral rallies. Small-cap funds emerged as standout performers, delivering returns in the range of 17–20%, reflecting renewed investor confidence after a period of caution. Several fund houses even reopened select small-cap schemes for lump-sum investments, signalling improved liquidity and sentiment. Sectoral and thematic funds also outperformed, benefiting from strong gains in industrial products, construction, and electrical equipment sectors, while large-cap and diversified funds offered relatively moderate but stable returns amid ongoing market volatility. A major highlight of April was the implementation of sweeping regulatory reforms by the Securities and Exchange Board of India through the new Mutual Fund Regulations 2026, effective from April 1. These reforms significantly enhanced transparency, governance, and investor protection. One of the most important changes was the restructuring of the Total Expense Ratio (TER), which is now unbundled into components such as Base Expense Ratio, brokerage, and statutory costs, making fund charges more transparent. Additionally, expense caps were slightly reduced, ensuring lower costs for investors. The regulations also introduced stricter rules for thematic and sectoral funds under a “true-to-label” framework, requiring greater portfolio differentiation to ensure genuine exposure. Another key structural shift was the introduction of Life Cycle Funds, a new category designed for long-term, goal-based investing, particularly retirement planning. These funds automatically adjust asset allocation from equity to debt as investors age, replacing older solution-oriented schemes like retirement and children’s funds, which are gradually being phased out. This marks a transition toward more flexible and investor-friendly products. April also saw continued innovation and expansion in product offerings. New Fund Offers (NFOs) from asset management companies, including hybrid index funds and multi-asset fund-of-funds, highlighted a growing emphasis on passive and diversified investment strategies. This reflects a broader industry trend toward cost efficiency and asset allocation-based investing. On the operational side, investor security received a boost with the introduction of features like the “folio lock” or voluntary debit freeze by major fund houses. This allows investors to temporarily block redemptions or withdrawals from their accounts, adding an extra layer of protection against fraud and unauthorized transactions. Despite global uncertainties, the industry demonstrated strong resilience. Total assets under management (AUM) remained robust, reaching around ₹73 lakh crore, supported by consistent Systematic Investment Plan (SIP) inflows exceeding ₹31,000 crore. However, the debt mutual fund segment faced pressure, with notable outflows driven by rising yields and tight liquidity conditions. Overall, April 2026 was defined by a combination of strong equity performance, regulatory transformation, and structural evolution. The industry not only delivered impressive returns but also laid the foundation for greater transparency, investor protection, and long-term growth through innovative products and reforms.